As you might imagine, one of the most often asked questions that I have received from clients is, “who will win the election, and what impact do you think that will have on the market?”

Clearly, I am without a crystal ball, and as the previous election reminds us, trying to out-guess the sentiment of voters can be a dicey proposition.

As I have mentioned before, the markets really don’t care who occupies the White House. The markets are neither Republican nor Democrat. Markets are driven by certainty, and they just want to know what the rules are. Clearly, those rules can change as a function of who occupies the White House.

Also, it seems that in advance of every election, there is a mindset of how this one will be the one that shapes the world forever. I would caution everyone to temper such thoughts. Elections are a normal part of our life, and the markets have always adjusted to those outcomes.

Having said that however, I do believe that this election will have an impact on the economy and by extension, the market as well. Within this article, I simply want to observe some quantifiable fact as it pertains only to matters of economic concern. This is not to be construed as a referendum on social issues, or other factors that can, and often do, shape an individual’s motivation for voting.

I’ll summarize my thoughts within this editorial, however for a more robust discussion about this topic, please find a few minutes to watch the video that you’ll find on both our website, and upon the Trussville Tribune website. I would like to focus on four main areas. First, we will focus on what we know about the difference in the tax policy of the two candidates, and in the process, we will take a look back to when we last saw a similar approach to taxation and economic policy.

Secondly, we will evaluate how that tax policy impacted the economy in terms of consumerism, as evidenced by the velocity of money. Third, we will take a look at how the differences in economic policy shaped consumer behavior in terms of increases to income, and the behavior of corporations with regard to decisions made with cash reserves.

Lastly, we will take a look at the stock and the bond markets themselves to see if we can glean any insight as to what the markets may be telling us at this time.

With less than two weeks before the election, we know that the Biden campaign has clearly stated the intent to seek the repeal of the Tax Cuts and Jobs Act. At a very high level, this means that the top corporate tax bracket could rise from 21% to 28%, and the top personal income tax bracket could rise from 37% to 52%. Small businesses could see their tax liability rise from 29.6% to 39.6% and those who invest could see taxes on dividends rise from 23.8% to 43.4%.

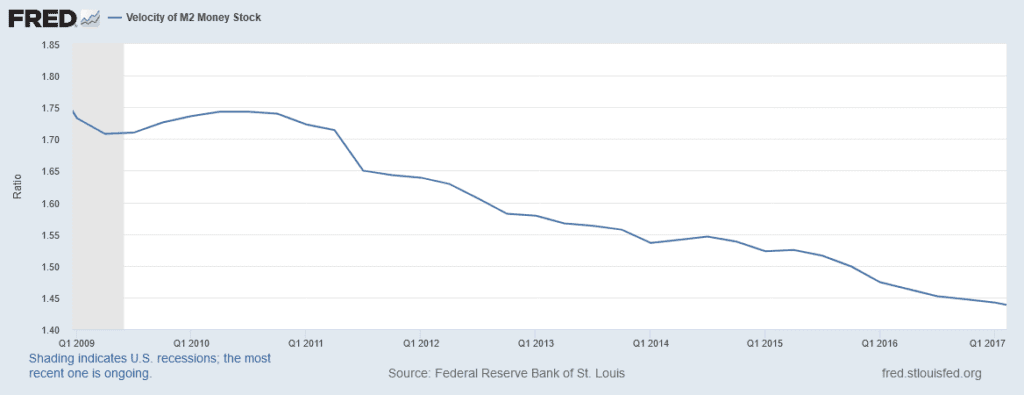

As we look back through history, its clear that a more onerous tax policy leads to a negative feedback loop of higher layoffs, slower wage growth, slower consumerism, and lower velocity of money.

Indeed, if we simply look back to the previous Obama / Biden Administration, when similar higher burdens of taxation were in place, we observed the velocity of money decline for eight consecutive years.

This, among other things, manifest in very slow growth of Gross Domestic Product. Indeed, the Obama / Biden Administration was the only Administration to never witness real annualized GDP growth higher than 2.6%. This data from the US Bureau of Economic Analysis, and it was published by CNN Money in January of 2017. We cover this in much more detail within our video.

Indeed, if you’ll Google “velocity of money”, you’ll find a definition from Investopedia that describes a low velocity as being a characteristic of slow economic growth, or recessions.

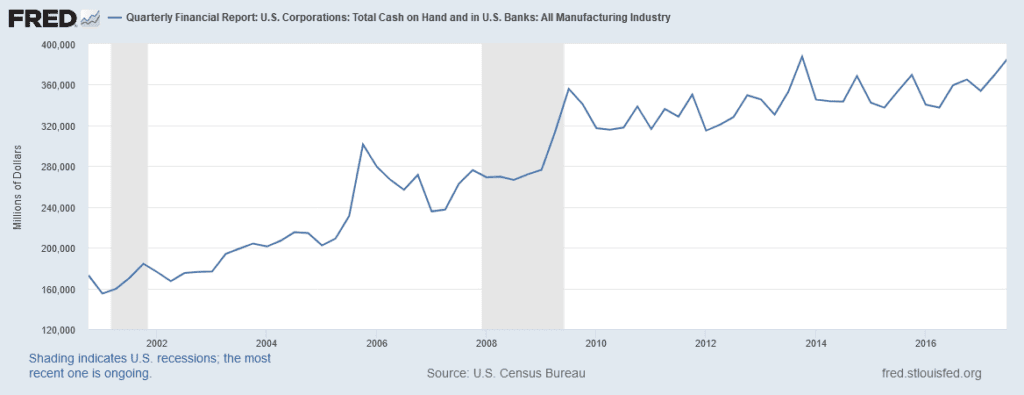

Gross Domestic Product wasn’t growing because consumerism was shunted, and this was due to the slow rate of jobs growth during this time, that resulted from the reluctance of corporations to spend money at a normal rate. There’s no need to expand plant capacity, and therefore no need of additional capital equipment to meet a declining demand for goods and services, and therefore no need for additional labor to run those machines that don’t exist, and hence the stagnation in wage growth. Do you see the connection?

Well, if you’re not spending cash, then you’re likely hoarding it, and this has been well documented over the last ten years. Consider this graphic from the Federal Reserve Bank of St. Louis that depicts the significant rise of cash on hand across US industrial companies over the eight years of the previous Administration, relative to the years of the Bush Administration.

By June of 2019 however, the Wall Street Journal published an article that described how stockpiles of cash on the balance sheets of US companies had fallen to a three year low. Again, please review our video for a much more detailed discussion of this trend.

The bottom line is that when the tax policy of an Administration changes dramatically, it often alters the behavior of corporations, and as a result, manifests in more robust economic activity. Over the last three years, we’ve observed this squarely in the heart of blue collar, middle America.

Within our video, we cover this in greater detail. Under the Bush Administration, US household median income grew by 0.7% per year. Under the Obama Administration, it grew by 1.7% per year. Under the first three years of the Trump Administration, it grew by 6.7% per year, and the primary catalyst was the Tax Cuts and Jobs Act. These numbers are well documented across many sources, but I’m citing the Heritage Foundation in this article.

This is important because as you’re contemplating the disposition of your long-term investments, we need to understand what the economic cycle might look like over the coming 12 to 48 months if we assume a dramatic change to policies of taxation and fiscal spending.

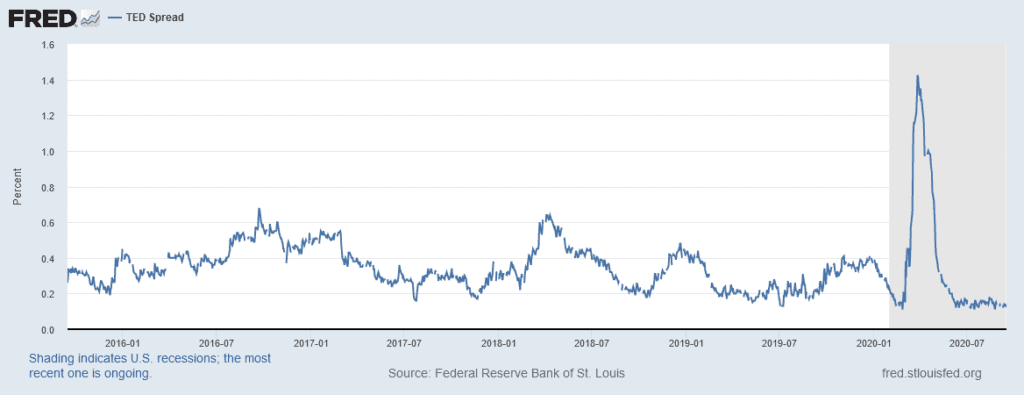

This is a graphic of the TED spread, and I’ve cited the importance of this metric within many previous writings and videos. The bottom line is that a tight spread indicates that the bond market sees strong present economic conditions, and the likelihood that those conditions will either remain strong, or strengthen, over the near term.

Observe that in January of 2016, the TED spread began to drift higher until peaking at 71 basis points in advance of the previous election, as assumptions of continuing slower growth were priced into both the stock and bond markets.

Following the election, the TED spread was halved by the end of 2016, and fell to 18 basis points by July of 2017. In my opinion, if the bond market believed that we were two weeks away from potentially returning to a tax and fiscal policy of the previous Administration, then we would likely not see a 14 basis point TED spread today. By extension, I also don’t believe that the Dow Jones Industrial Average would be above 28,000 either. Markets have seemingly priced into themselves the assumption of robust growth, not tepid growth. Markets are discounting mechanisms. Given that observation, if the stock and bond markets sensed that a dramatic change in tax and fiscal policy was upon us, I believe we would have already observed that in the TED spread and market valuations.

Lastly, many corporations are surprisingly reporting the presence of positive free cash flow at this time. Given the proximity to the re-opening of the economy, I wouldn’t have expected that so quickly. What’s even more surprising however is that many of these companies are describing plans of increasing dividend payments. Knowing that we observed the willingness to hoard cash under the tax and fiscal policies of the previous Administration, again, if corporate America held the belief that we were less than two weeks away from going back to a similar structure, then I doubt we would be hearing about plans to send free cash flow out the door in the form of higher dividend payments.

So, in summary, based on everything that I’ve mentioned here, and that we observed in our recently published video, it is my belief that neither the stock market, nor the bond market, nor corporate America for that matter seems to assume that we will have a change in current economic and tax policy, as evidenced by behavior and quantifiable metrics.

Read into that what you will, but I believe I have presented numbers with which there is no argument, and trends that can be clearly observed. Having said that, remember that for most of you, investment objectives that are longer-term in nature are in a position to survive the impending election result. Yes, it is possible that tactical changes may be necessary to long-term investment plans, but rarely does that mean the cessation of those plans. Remain true to your investment goals, take advantage of opportunities that the market provides to you, and be mindful of quantifiable fact, and insulate yourself from national media sensationalism.