It is. Most people don’t feel it however. This isn’t a data issue. It’s a duration issue. Our capacity to consume has only been imperially positive over the last three months. Well, three points of data will not outweigh thirty-six points of data.

It is. Most people don’t feel it however. This isn’t a data issue. It’s a duration issue. Our capacity to consume has only been imperially positive over the last three months. Well, three points of data will not outweigh thirty-six points of data.

I need to see 15 more of these data points where inflation is lower than the degree by which our incomes are rising before I can have confidence that attitudes toward consumption might change. Indeed, Dr. David Kelley recently observed that we have a bottom decile attitude toward a top quartile economy.

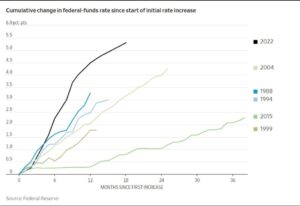

I believe market participants were expecting a longer and more tepid approach to the removal of accommodation, similar to what we experienced in the 2015 tightening cycle. What we got was Paul Volker 2.0 and the most aggressive Fed in forty years. This was a shock to the markets. The greater the magnitude of the shock, the longer it takes from which to recover.

I believe market participants were expecting a longer and more tepid approach to the removal of accommodation, similar to what we experienced in the 2015 tightening cycle. What we got was Paul Volker 2.0 and the most aggressive Fed in forty years. This was a shock to the markets. The greater the magnitude of the shock, the longer it takes from which to recover.

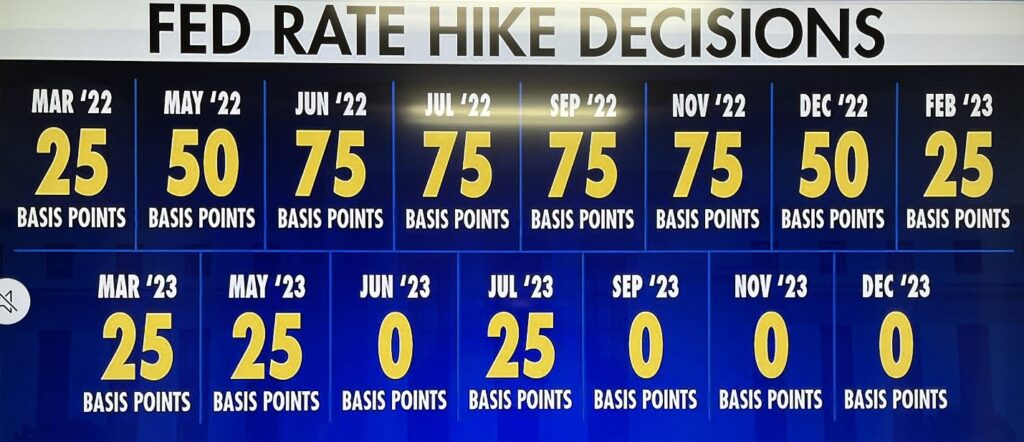

So, the question becomes, has the Fed done exactly what they said they were going to do? Yes, I believe so. In November of last year, Chairman Powell told us that the Fed would be less hawkish, more data driven, and judicious with future policy decisions.

Well, it looks like they’ve done just that. By the numbers, it’s even more evident, but I don’t think that fixed income or equity market participants actually believed it, until possibly, just now.

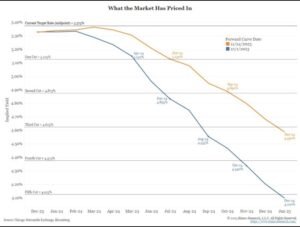

Looking at this chart, it would appear that by the actions of treasury market participants, there is now a discernable shift, just since Thanksgiving, about where market participants believe future Fed policy decisions may land next year.

The Fed has been conveying the same message now for thirteen months. Seemingly, only now has the treasury market heard it. I think this is a positive development as we launch into the new year.

The Fed has been conveying the same message now for thirteen months. Seemingly, only now has the treasury market heard it. I think this is a positive development as we launch into the new year.

Throughout the year, I’ve spoken about how in my opinion, the market is broadly undervalued, and seemingly being led by a narrow basket of AI thematic companies. Indeed, that remains true. I can’t get into a discussion of specific stocks of companies in an article such as this, however I do believe that the overwhelming majority of the market remains very attractively priced when viewed from a forward PE perspective, and other metrics.

Recently, I found this stochastic view of the market.

At a high level, stochastic analysis is simply observing points of strength and resistance, and then connecting those dots to form Bollinger bands. When you hear that markets are bouncing off of strength or running into resistance, it is to these Bollinger bands to which reference is being made.

Looking at this graphic, it would appear that a cone convergence is underway. That’s exciting in and of itself, but it’s even more exciting to see that the fifty-day moving average, and the two hundred day moving average and the current valuation of the market are seemingly converging at the same time. Something is about to happen.

Any good stochastician would tell you that if you breech a Bollinger band and close above or below that level, there is a good probability that you’ll establish that resistance or support level at 10% to 15% higher or lower than the previous level.

Well, notice the blue line, and where the S&P Index was just three weeks ago, as it was flirting with that upper-level resistance. Since then, we’ve heard from Chairman Powell following the December Fed meeting, and the market closed well above that upper level of resistance.

That’s a good technical indicator if you’re into such things, that we might be positioning ourselves for a reasonably green 2024.

There are no ringing bells or alarms to signal when palpable sentiment begins to dissipate. Which is why you must find the intestinal fortitude to be this guy, the jet fighter pilot on vacation when it comes to resisting the urge to succumb to sensationalism and speculation. Rise above, think outside of the box, and remain focused on the long term and the fruition of planning goals.

There are no ringing bells or alarms to signal when palpable sentiment begins to dissipate. Which is why you must find the intestinal fortitude to be this guy, the jet fighter pilot on vacation when it comes to resisting the urge to succumb to sensationalism and speculation. Rise above, think outside of the box, and remain focused on the long term and the fruition of planning goals.